RWA Tokenization Technology Analysis: What Are the Current Solutions?

Original Title: "Technical Analysis of Real World Asset (RWA) Tokenization Mechanism"

Original Source: Aquarius

Tokenized Real World Assets (RWAs) are digital tokens recorded on the blockchain, representing ownership or legal rights to physical or intangible assets. The scope of tokenization covers a wide range of asset classes, including real estate (residential, commercial properties, and Real Estate Investment Trusts REITs), commodities (gold, silver, oil, and agricultural products), art and collectibles (high-value art pieces, rare stamps, and vintage wines), intellectual property (patents, trademarks, and copyrights), and financial instruments (bonds, mortgages, and insurance policies).

By enabling fractional ownership, tokenization enhances asset liquidity, making investment opportunities that were once exclusive to high-net-worth individuals and institutional investors more accessible to the general public. The blockchain's immutable ledger ensures transparent ownership records, reducing fraud risks; simultaneously, tokenized assets traded on decentralized exchanges bring unprecedented market accessibility and efficiency.

According to McKinsey's analysis, it is estimated that by 2030, the total market value of various tokenized assets (excluding cryptocurrencies and stablecoins) will reach around $20 trillion, with a pessimistic scenario of $10 trillion and an optimistic scenario of $40 trillion. These estimates do not include stablecoins (including tokenized deposits, wholesale stablecoins, and Central Bank Digital Currencies CBDCs) to avoid double counting, as these instruments are commonly used as cash payment tools in tokenized asset transactions.

Current System

Tokenization of real-world assets refers to representing off-chain assets' ownership in digital token form through blockchain or similar distributed ledger. This process links the asset's characteristics, ownership, and value to its digital form. Tokens, as digital holding instruments, enable their holders to claim ownership of the underlying assets.

Historically, physical ownership certificates were used to prove asset ownership. While useful, these certificates were vulnerable to theft, loss, forgery, and money laundering threats. In the 1980s, digital holding instruments emerged as a potential solution. However, limited by the computing power and encryption technology of that time, these tools were not realized. Instead, the financial industry turned to centralized electronic registry systems to record digital assets. Although these paperless assets brought some efficiency gains, their centralized nature required the involvement of multiple intermediaries, introducing new costs and inefficiencies.

System Based on Distributed Ledger Technology

The development of Distributed Ledger Technology (DLT) has made it possible to reconsider the concept of digitally holding securities or tokens.

DLT consists of a series of protocols and frameworks that allow computers to propose and validate transactions on a network while maintaining the synchronicity of records. By storing records in a decentralized manner, this technology shifts responsibility away from a single central authority. Such decentralization reduces administrative burdens, minimizes the risk of system failures associated with reliance on a central entity, making the system more resilient (see Figure 1).

These diagrams compare the transaction flow between traditional systems and DLT-based systems. Figure 1 illustrates how multiple intermediaries in the current system handle transaction execution, clearing, and settlement. Figure 2 shows how DLT-based systems streamline these processes through a single consensus mechanism.

Decentralized Solutions

Blockchain is a type of Distributed Ledger Technology that operates through a decentralized computer network. Tokens can be issued on two types of blockchains: private permissioned chains and public permissionless chains.

Private permissioned chains (e.g., Ripple) are controlled by a single entity and restrict access to specific users, creating a controlled ecosystem. Public permissionless chains (e.g., Ethereum), on the other hand, do not require central authority control and provide open access to all users. When tokens are issued on public permissionless chains, they can integrate with decentralized finance (DeFi) protocols (such as decentralized exchanges), enhancing their utility and value.

The choice of blockchain—whether in a private controlled environment or a public open network—determines the level of control the issuer can maintain over the tokens. Compared to private permissioned chains, public permissionless chains give the issuer less control. The choice of blockchain architecture should align with the issuer's goals and the expected functionality of the tokens.

A key advantage of asset tokenization is the automation achieved through smart contracts. Smart contracts are programs on the blockchain that execute when specific conditions are met. These contracts automate financial transactions and administrative tasks, reducing the need for manual work and intermediaries. By eliminating counterparty risk, this automation makes operations more efficient and secure, enabling faster and lower-cost transfers.

Tokenization Approaches

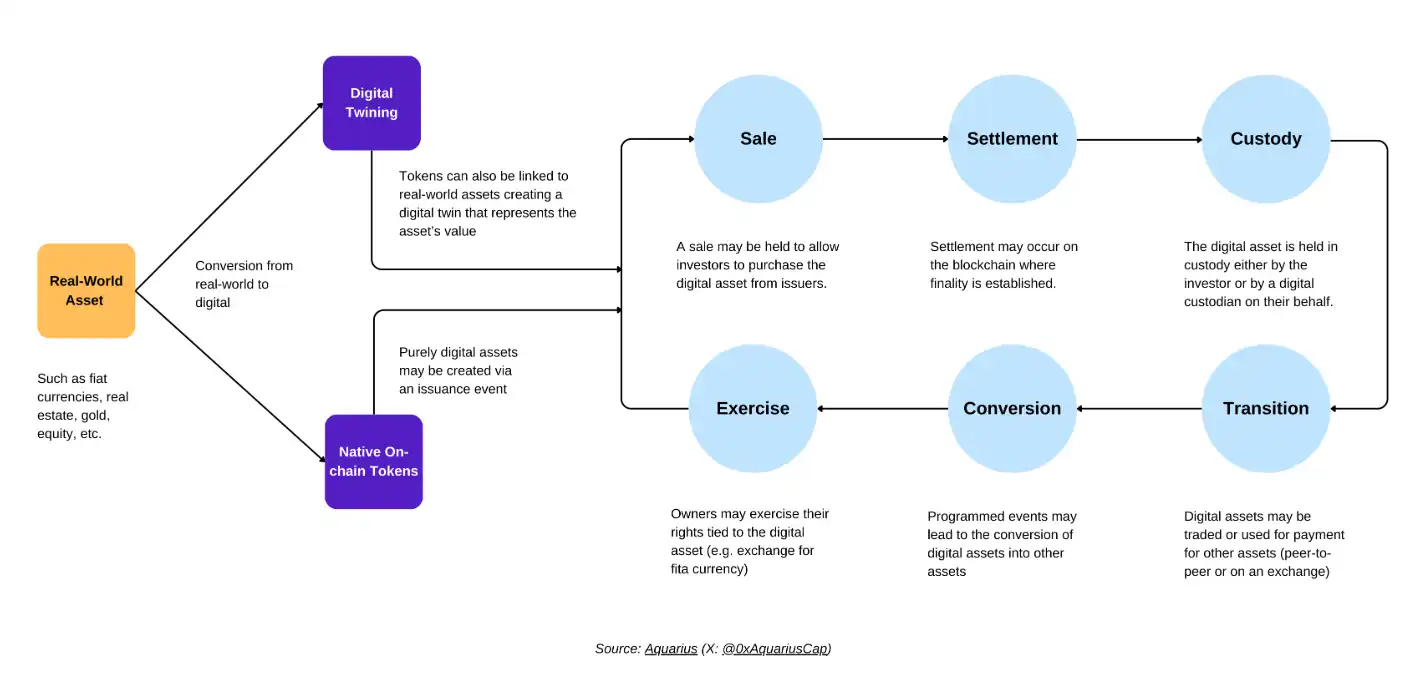

The tokenization of real-world assets has traditionally been approached with a simple binary classification: an asset is either tokenized or it is not. However, as we enter the era of digital assets, this overly simplistic view no longer applies. A more nuanced way is to analyze assets through two key attributes: their form and ownership.

The form includes the asset's economic characteristics—its function, underlying asset, maturity date, and interest rate. Additionally, ownership validation requires a ledger, which can be off-chain or on-chain. Off-chain assets maintain their rights and form through physical certificates (such as holding a bond) or dematerialized form (such as electronic record of shares), all operating within a legal framework. On the other hand, on-chain assets exist in a digitally enhanced or digitally native form, managed by a blockchain's consensus mechanism.

Understanding the difference between digitally enhanced assets and digitally native assets is crucial. Digitally enhanced (or enhanced) assets maintain ownership through an off-chain ledger as their custody layer while using blockchain tokens as the digital form. For example, ownership of a stock may exist in an electronic ledger but is tokenized on a blockchain to enhance its functionality. In contrast, digitally native assets (such as cryptocurrencies) are inherently digital, with tokens directly representing value and ownership. This means that while a token of a digitally enhanced asset provides a claim to ownership from an off-chain ledger, a token of a digitally native asset directly represents ownership without relying on any off-chain components.

Building on an understanding of asset types and tokenization, we can further explore four tokenization approaches. The differences in these approaches lie in the direct relationship between the token and its underlying asset. Next, we will systematically discuss each approach, from the most direct relationship between token and asset to the least direct relationship.

· Direct Ownership: In this approach, the digital token itself acts as the official ownership record, eliminating the need for a custodian. This method is applicable only to digitally native assets (see Figure 2). The system uses a single ledger (potentially a distributed ledger) to record token ownership. For instance, rather than issuing tokens supported by a share registry system, it is more direct to tokenize the registry system itself, making the token the actual ownership record. This streamlined approach eliminates the need for custodians or redundant registries. While this method can leverage a distributed ledger, the registry system itself does not necessarily need to be distributed. However, the legal frameworks for most asset classes under this tokenization method are still limited, and the regulatory structures are not yet mature.

· 1:1 Asset-Backed Tokens: In this approach, a custodian holds the asset and issues tokens representing a direct interest in that underlying asset. Each token can be redeemed for the actual asset or its cash equivalent. For example, a financial institution can issue bond tokens based on bonds held in a trust account, or a commercial bank can issue stablecoin tokens backed one-to-one by commercial bank currency in a dedicated account.

· Collateralized Tokens: This method issues asset-backed tokens using assets that differ from the expected representation of the asset or related equity as collateral. Typically, to mitigate the fluctuation in collateral asset value relative to the expected token asset value, the token is over-collateralized. For example, the stablecoin Tether is backed not only by cash but also by a range of other assets (such as fixed-income securities). Similarly, one could create a government bond token backed by commercial bank bonds or a stock token backed by an over-collateralized basket of related stocks.

· Under-collateralized Tokens: Tokens issued using this method are designed to track the value of an asset but are not fully collateralized. Similar to a fractional reserve banking system, maintaining the token's value requires managing a partial reserve asset portfolio actively and engaging in open-market operations. This is a form of high-risk asset tokenization, with historical cases of failures. For example, the collapsed Terra/Luna stablecoin was not independently asset-backed but relied on an algorithmic stabilization through a supply control algorithm. Other less risky partially collateralized tokens have also been issued.

Why Choose Tokenization

The tokenization of real-world assets primarily leverages Distributed Ledger Technology (DLT) to achieve efficiency gains. This technology enhances transparency, automates processes, reduces operational costs, eliminates intermediaries, and counterparty risks. Compared to traditional financial systems, these advantages are realized through a streamlined and agile market infrastructure, resulting in faster settlements and cost savings.

· Atomic Settlement

The combination of Distributed Ledger Technology with tokenized assets introduces the concept of atomic settlement. Currently, settlements mainly occur through central counterparties, and the prevalent securities settlement mode is the rolling settlement cycle. In this mode, although transactions are executed on a specific day, the actual settlement (transferring ownership according to the agreed protocol) often takes one to three more days to complete. This involves two legs or transfers: the delivery leg, transferring ownership of securities from the seller to the buyer, and the payment leg, transferring cash from the buyer to the seller. Atomic settlement is achieved through smart contracts, where the programmable code simultaneously executes both legs of the transaction or does not execute at all if the predetermined conditions are not met. This method eliminates counterparty risk while significantly enhancing transaction speed and efficiency. Moreover, conducting trade settlement through smart contracts eliminates the need for collateral since there is no risk of delivery failure and subsequent trade reconciliation, thereby freeing up collateralized funds and indirectly boosting market liquidity.

· Increased Liquidity

Tokenization has significantly enhanced the transferability of assets, making previously illiquid assets tradable. For example, traditional real estate transactions face significant barriers such as high transaction costs, complex legal processes, and inherent illiquidity. These barriers, coupled with each property's unique attributes (such as location, condition, legal status), make trading individual properties like stocks or bonds on a public exchange impractical. Tokenization addresses these challenges through smart contracts, which optimize the transaction process by eliminating intermediaries, streamlining ownership transfers, and automating compliance checks, thus significantly reducing transaction costs. The same benefits apply to other traditionally illiquid assets such as art, collectibles, infrastructure projects, and private equity shares. Additionally, tokenization has enabled new distributed markets through Automated Market Makers (AMMs). These systems automatically match buyers and sellers through asset pools managed by smart contracts, providing continuous liquidity. Unlike traditional markets with fixed trading hours, these blockchain-based systems operate 24/7. Higher accessibility is further enhanced through fractional ownership, lower investment thresholds, and simplified transaction processes.

· Reduction in Intermediation

The decentralized data structure allows smart contracts integrated on the blockchain to replace traditional intermediaries in data verification. Smart contracts can also replace Central Securities Depositories (CSDs), automating processes such as asset ownership transfers, dividend payments, and interest distributions.

· Enabling Automation

One of the key advantages of asset tokenization is enabling automation through smart contracts. Smart contracts are programmable code deployed on the blockchain that automatically execute when predetermined conditions are met. Smart contracts can streamline many manual tasks, especially in industries like insurance. For example, they can automate policy issuance and claims payments. In case of flight delays or cancellations, smart contracts can automatically trigger travel insurance payouts without manual intervention. The effectiveness of such automation largely depends on integrated and real-time monitoring of relevant data. Third-party services known as "oracles" provide external data to smart contracts, serving as a bridge between the blockchain and the outside world since smart contracts cannot access external data directly. Automation is most feasible in asset classes that are data quantifiable, standardized, and reliably obtainable through oracles. Stocks, bonds, and derivatives are prime examples as their market data is readily available and easily integratable into smart contracts. However, in industries where data subjectivity is high or difficult to quantify, automation faces greater challenges. For instance, real estate involves complex transactions requiring manual verification of legal documents, subjective property assessments, and compliance with diverse regulatory frameworks—making comprehensive automation via smart contracts more challenging.

· Facilitating Compliance

Compliance is a key aspect of tokenized assets. With the development of regulatory frameworks such as Know Your Customer (KYC), Anti-Money Laundering (AML), and Countering the Financing of Terrorism, a more secure environment has been created for digital finance and transactions. The underlying technology of tokenized assets makes compliance with these requirements more efficient and standardized through standardization and automated processes.

KYC and AML regulations can be directly encoded into the blockchain or individual asset transfer rules, enabling more efficient interactions. For example, when a customer establishes a relationship with a new financial institution, their identity information can be automatically transferred with their consent. Research on the impact of tokenization on banking infrastructure has shown positive results. By analyzing over 50 operational cost metrics, the study found that improved auditability and transaction transparency can reduce overall compliance costs by 30% to 50%.

· Automated Market Makers (AMMs)

Smart contracts are revolutionizing traditional market-making mechanisms through Automated Market Makers (AMMs). Traditional market makers provide liquidity by acting as buyers and sellers of securities, while AMMs take a different approach. They use smart contracts to automatically match buyers and sellers using asset pools provided by liquidity providers. These blockchain-embedded smart contracts algorithmically determine asset prices and manage asset pools. The automation features of AMMs significantly reduce costs and improve performance. Research has shown that compared to traditional systems, AMMs have significantly lower transaction costs, especially excelling in high-volume and low to medium volatility assets.

Risks and Costs of RWA Tokenization

Despite the many advantages that tokenized assets bring, their adoption still faces significant challenges. The main risks come from technological and regulatory considerations. Technology-related concerns include cybersecurity vulnerabilities, system scalability limitations, settlement processes, network stability, and efficiency issues. On the regulatory front, key issues involve AML compliance, governance frameworks, identity verification, and data protection and privacy. Researchers suggest that addressing digital asset regulatory issues should not be limited to just integrating new technology into existing frameworks. Instead, we should explore how to leverage blockchain technology and smart contracts to enhance regulatory compliance.

In addition to technological and regulatory challenges, investor behavior and market dynamics bring additional complexity. Achieving widespread adoption requires a significant amount of education and awareness efforts. Market risks include the potential overvaluation of assets due to speculative trading and increased price volatility due to the digital nature of these assets. Furthermore, the high energy consumption of blockchain consensus mechanisms has raised environmental concerns. To fully realize the advantages of tokenization in the financial sector, these multifaceted challenges must be addressed.

The transition to a tokenized financial system involves significant costs. Among the most notable expenses are those stemming from the infrastructure changes required to support blockchain and tokenization technology. Organizations need to invest in a secure, scalable blockchain platform, acquire specialized software to manage tokenized assets, and provide training to employees to adapt to these new systems. Integration costs are equally significant—there is a need to connect these new systems to existing financial infrastructure while maintaining security and operational integrity. Educational efforts to increase understanding and overcome skepticism also pose a significant direct and opportunity cost for governments. Lastly, the high energy consumption of blockchain consensus mechanisms presents a dual financial and environmental challenge.

Disclaimer: This article is for general information purposes only and does not constitute investment advice, recommendation, or an invitation to buy or sell any securities. This article should not be relied upon as the basis for any investment decision, nor should it be used as a basis for accounting, legal, tax, or investment advice. It is recommended that you consult your own advisors on legal, business, tax, or other matters related to any investment decision. Some information contained in this article may be from third-party sources, including portfolio companies of funds managed by Aquarius. The views expressed in this article are solely the author's personal opinions and do not necessarily reflect the position of Aquarius or its affiliates. These views may change at any time without notice and may not be updated.

Original Article Link

You may also like

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

Should we escape the peak? The principle of the tail-end market in the stock market

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.